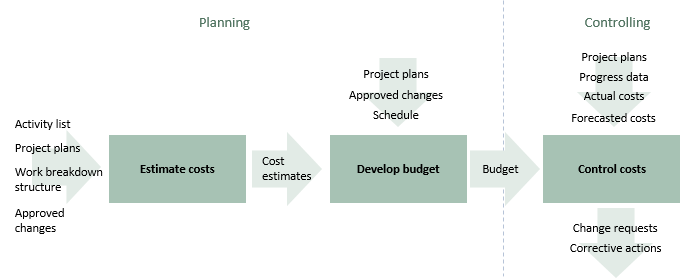

The ISO21500 cost subject area contains three processes.

| ISO21500 process groups | |||||

|---|---|---|---|---|---|

| Initiating | Planning | Implementing | Controlling | Closing | |

Cost | 4.3.25 Estimate costs 4.3.26 Develop budget | 4.3.27 Control costs

| |||

In the diagram below, these processes are presented as a flow diagram using the inputs and outputs defined in ISO21500. There are two planning processes and one controlling process.

Click on the diagram for more detail on each process.

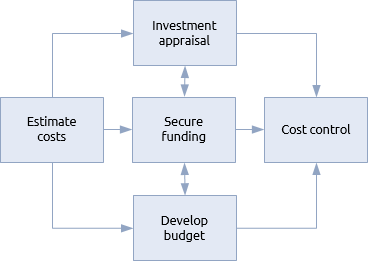

The corresponding financial management procedure from Praxis is shown below. It should be noted that the Praxis financial management function is broader than ISO21500’s cost area as it also includes investment appraisal and funding.

The purpose of this process is to develop an approximate cost of individual activities and the project or programme as a whole. ISO21500 points out that on long term projects and programmes, costs that are well into the future may need to have the ‘time value of money’ taken into account (e.g. the use of disconted cash flows).

The equivalent procedural step in Praxis is estimate costs.

Another sophisticated approach is to take account of learning curves for repetitive activities – something that would also have an impact on the estimation of activity durations and resource requirements.

Estimates will be regularly revisited in the light of approved changes and progress information.

Estimates are, by definition, an inaccurate forecast of the eventual cost of an activity or project. The degree of inaccuracy will depend upon risk and uncertainty. Cost reserves should be added to the estimates to create a budget that accommodates identified risks (contingency reserve) and general uncertainty (management reserve).

The equivalent procedural step in Praxis is develop budget.

The budgeting process also allocates funds to different elements of the project or programme so that performance can be managed. In addition to the contingency reserve and management reserve, there may also be a reserve to cover approved change requests.

Once work is started progress data are accumulated and the actual costs are compared to the budgets (baseline costs) so that appropriate corrective action can be taken.

The equivalent procedural step in Praxis is cost control.

Tolerances must be set so that every minor deviation from the baseline doesn’t trigger corrective action. If tolerances are exceeded, a recovery plan may be required and if costs cannot be held within the current budget, it may be necessary to secure additional funds and reset the baseline.

This will be governed by the control change process and result in an approved change – which feeds into the first process in this sequence.