Where are we?

You are well into definition. You have produced your draft milestone schedule and detailed project schedule and you have enhanced this by applying some risk management activities. You are now ready to calculate the project budget.

Do we really need to do this?

This is an excellent question to start with. Not every project needs to have a separate budget calculated and managed, as many smaller projects are run within the operating budget of the relevant department or team. In these circumstances maybe no detailed budget management is required.

In fact, there is a series of potential levels of budget management, as follows:

-

The project will operate entirely within the operational budget, and no separate account needs to be created for the project budget.

-

You will need to estimate and manage the expenditure, but only on external resources (outside your organisation), as this involves us spending real money.

-

You will need to estimate and track all expenditure on capital items (things you will purchase during the project), as these may have tax, depreciation, grant and corporate accounting implications.

-

You will need to estimate and track every last piece of money spent on this project, as we will charge the customer for the work, and we must make a profit (or, at least, not make a loss)

-

You will need to estimate and track every last piece of money spent on this project, as the company standard is to have this level of financial control on all projects over (say) €50,000.

You must ask the project sponsor (and maybe your boss, and maybe a company expert – see below) for guidance on what you need to calculate, how you should present it, and how you should record and report it.

It is worth finding out who in your organisation is the expert in this sort of thing. You will not be the first person to calculate a project budget and someone will already have established useful things, such as the standard daily cost of a full-time employee and so on. This person may be the one who has to sort out any mess you make, so it may be as well to get them involved from the outset!

What does a budget look like?

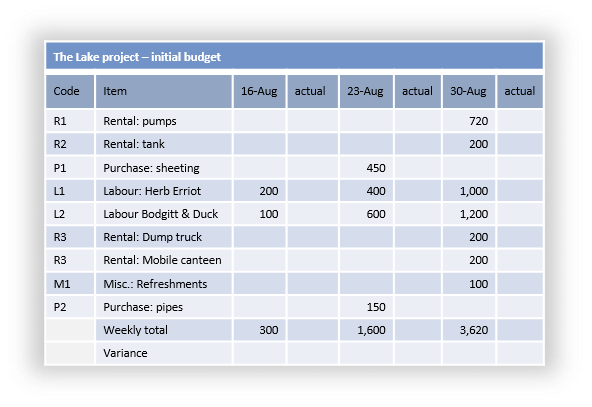

It is usual to show the costs against the time period in which they are consumed, not when they are actually paid (which, in the case of outside suppliers may be several months later).

Project costs are often shown in the same scale and format as the schedule, i.e. on a weekly or monthly chart. It is possible to draw the equivalent of a Gantt chart or schedule that shows costs incurred as opposed to units of resource allocated to activities.

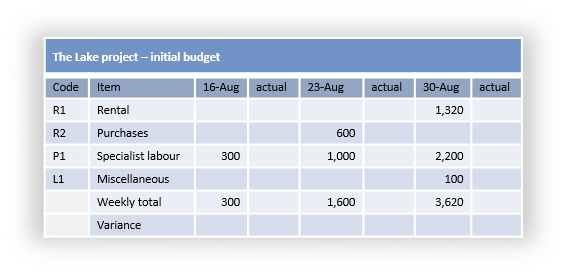

Many sponsors will not want to be bothered with every tiny detail (until things go wrong!), so it may be useful to produce a summary for publication as shown below. You should keep detailed records for your own day-to-day management as well.

Where do the numbers come from?

Of course, how the budget is presented is all very well, but if the numbers are inaccurate then no amount of dressing up and fancy presentation will obscure this fact.

Actually most of the budget numbers come as a by-product of your detailed planning work. The elements of a budget are as follows:

-

Labour costs: and you can see this easily on your schedule, as you now know exactly who will be involved, and for how long

-

Purchases: ditto, from the schedule

-

Rental: ditto, from the schedule

-

Travel and subsistence: this might need a little thought, but based upon the schedule you will be able to see where the work must be carried out, and you can calculate likely travel and subsistence costs, probably based upon your company standard rules.

-

Project management activity: this must be included and will cover all your time to plan, monitor, replan and report, risk and stakeholder management activities and an allowance for team management time.

-

Contingency allowances: this may vary from one organisation to another. Some companies will want to see a contingency allowance, others will not.

You can see that you have already identified all of these items as part of your definition work, hence the suggestion that a project budget is a by-product of other planning activity.

You will be able to use these budget figures to monitor the expenditure and report budget status to the sponsor. This control aspect is covered in the chapter on controlling progress.

Summary

Find out just what you need to estimate and track by asking your sponsor or boss. Also agree on the way in which you can summarise the information when reporting. Develop detailed weekly or monthly budget figures, and then summarise appropriately.

Checklist

Discuss and agree the scope and level of detail you will have to keep | And find out the company standards for presentation formats |

Extract the detail from your project schedule | Again, using company standard costs for daily labour rates etc. |

Summarise into appropriate categories | And use this summary for all reporting to the sponsor |

Further reading

These links to the Praxis web site explain how the concepts introduced in this chapter can be applied to projects that involve more people and more complex relationships.

An overview of budgeting for more complex projects and programmes | |

A useful way to show cumulative expenditure, even on a very simple project |

Thanks to Mike Watson of Obsideo for providing this book